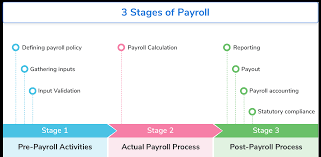

A payroll cycle is the recurring process that an organization follows to pay its employees. It includes various steps and activities that are typically carried out on a regular basis, such as weekly, bi-weekly, or monthly, depending on the organization’s payroll schedule. The primary purpose of a payroll cycle is to ensure that employees receive their wages accurately and on time. Here are the typical steps in a payroll cycle:

Timekeeping: Employees record their work hours, whether through timecards, electronic systems, or other methods. This data is used to calculate their wages.

Data Collection: Relevant payroll data is collected, including hours worked, overtime, bonuses, and any deductions (such as taxes and benefits).

Payroll Processing: Payroll staff or software systems process the collected data to calculate each employee’s gross pay, deductions, and net pay.

Tax Withholding: Payroll departments withhold the necessary federal, state, and local income taxes, as well as Social Security and Medicare taxes from employees’ paychecks. These withheld taxes are then remitted to the appropriate government authorities.

Deductions: Deductions for benefits, insurance, retirement contributions, and other deductions are processed and subtracted from the gross pay.

Direct Deposits and Paychecks: Employees are paid through direct deposit, paper checks, or other payment methods. Payroll staff ensures that the correct amounts are paid to each employee.

Pay Stubs: Pay stubs or statements are provided to employees, showing detailed information about their earnings, deductions, and net pay.

Reporting and Record-Keeping: Employers are required to maintain records of payroll transactions for tax and compliance purposes. They also need to file various reports with government agencies.

Compliance: Ensuring that the organization complies with all relevant labor laws, tax regulations, and other legal requirements is an essential part of the payroll cycle.

Reconciliation: Periodic reconciliation is performed to ensure that the payroll figures match with the financial records of the organization.

Distribution of Paychecks or Deposits: Payroll staff distributes paychecks or ensures that direct deposits are made into employees’ bank accounts.

Payroll Reporting: Employers must file payroll tax reports, W-2s, 1099s, and other forms with the appropriate government agencies.

Payroll cycles may vary in frequency, with some organizations processing payroll weekly, bi-weekly (every two weeks), semi-monthly (twice a month), or monthly. The specific steps and procedures in a payroll cycle can also vary depending on the organization’s size, industry, and location, as well as legal and regulatory requirements. Accurate and timely payroll processing is crucial to employee satisfaction and legal compliance.

Payroll:

Purpose: Payroll is primarily concerned with compensating employees for their work. Its main function is to calculate and process employee wages or salaries, along with any associated deductions and benefits.

Key Activities:

Recording and tracking employee hours worked.

Calculating gross pay, which is the amount employees earn before deductions.

Deducting taxes (e.g., income tax), Social Security, and Medicare.

Managing deductions for benefits (e.g., health insurance, retirement plans).

Ensuring employees are paid accurately and on time.

Compliance with labor laws and regulations.

Frequency: Payroll is typically processed on a regular schedule (e.g., weekly, bi-weekly, monthly).

Finance:

Purpose: Finance, often part of the organization’s broader financial management, focuses on the overall financial health and strategy of the company. It is concerned with managing and optimizing financial resources, budgeting, financial planning, and reporting.

Key Activities:

Financial planning and forecasting.

Budgeting and cost control.

Managing the organization’s financial assets, liabilities, and investments.

Reporting on financial performance and health.

Strategic financial decision-making.

Compliance with financial regulations and accounting standards.

Frequency: Finance activities are ongoing and may involve periodic reporting (e.g., monthly, quarterly, annually).

In summary, while payroll is a specific process that deals with compensating employees, finance encompasses a broader set of activities related to managing an organization’s financial resources, making strategic financial decisions, and ensuring compliance with financial regulations. These two functions work together to ensure that employees are compensated accurately and that the organization’s financial health is well-managed.

Gross Pay: The total amount of money an employee earns for their work, which is usually based on their hourly or salaried rate and the number of hours worked during the pay period.

Deductions: The amounts that are subtracted from an employee’s gross pay. Deductions can include income taxes, Social Security and Medicare taxes, retirement contributions, health insurance premiums, and other benefits or obligations.

Net Pay: The final amount an employee receives after all deductions have been subtracted from their gross pay. Net pay is the amount that employees take home as their actual compensation.

Additional Compensation: This may include bonuses, commissions, or any other extra payments that are due to employees for reasons such as meeting performance goals.

Processing payroll ensures that employees are accurately compensated and that all legal and regulatory requirements, including tax withholding and reporting, are met. It is a critical function for any organization to maintain employee satisfaction and comply with labor and tax laws.